5 Lessons The U.S. Can Learn From These Countries

The home healthcare industry has experienced exponential growth in the past few years. This is due to the rise in the aging population and the realization by many stakeholders that home care is more economical and provides a better health outcome for the patient.

About 70% of people who use home healthcare services are reportedly aged sixty-five and older. In this age group, the most common medical conditions requiring home care are heart disease, diabetes, and cerebrovascular diseases.

However, over one-third of those who receive in-home care and are under the age of sixty-five, are mostly diagnosed with various chronic health conditions that require targeted forms of assistance that can safely be given outside of a medical facility.

The concept of home healthcare has evolved over the years and is likely to play an integral role in shaping the future of healthcare in the U.S.

This article will highlight some incredible statistics that shed light on the state of home healthcare in three prominent countries—the United States, the United Kingdom, and Canada. These data points provide valuable insights for policymakers, healthcare professionals, and individuals seeking to understand and improve home-based healthcare services.

It will then conclude by pointing out five lessons that the United States can learn from these countries to improve the home healthcare sub-sector.

Home HealthCare Industry Stats: USA vs UK vs Canada.

Home Healthcare Market Size

The global home healthcare market size was valued at USD 362.1 billion in 2022 and is expected to grow at a Compound Annual Growth Rate (CAGR) of 7.96% during the forecast period from 2023 to 2030.

Research conducted in 2022 by Grand View Research valued the size of the US home healthcare market at $142.9 Billion while another one conducted by Insights10 valued the UK’s and Canada’s market size to be $9.429 billion and $29 Billion respectively.

Market Growth Rate

The growth rate of the industry in the U.S is projected to develop at a Compound Annual Growth Rate (CAGR) of 7.48%, the UK’s growth rate will exhibit a CAGR of 5.93% and Canada’s growth rate will be at a CAGR of 7.93%.

Revenue Forecast

According to SPER Market Research and Insights10, the US, UK, and Canada’s home healthcare market are projected to reach $322.82 billion by 2033, $14.494 billion by 2030, and $53 billion by 2030, respectively.

Employment and Workforce

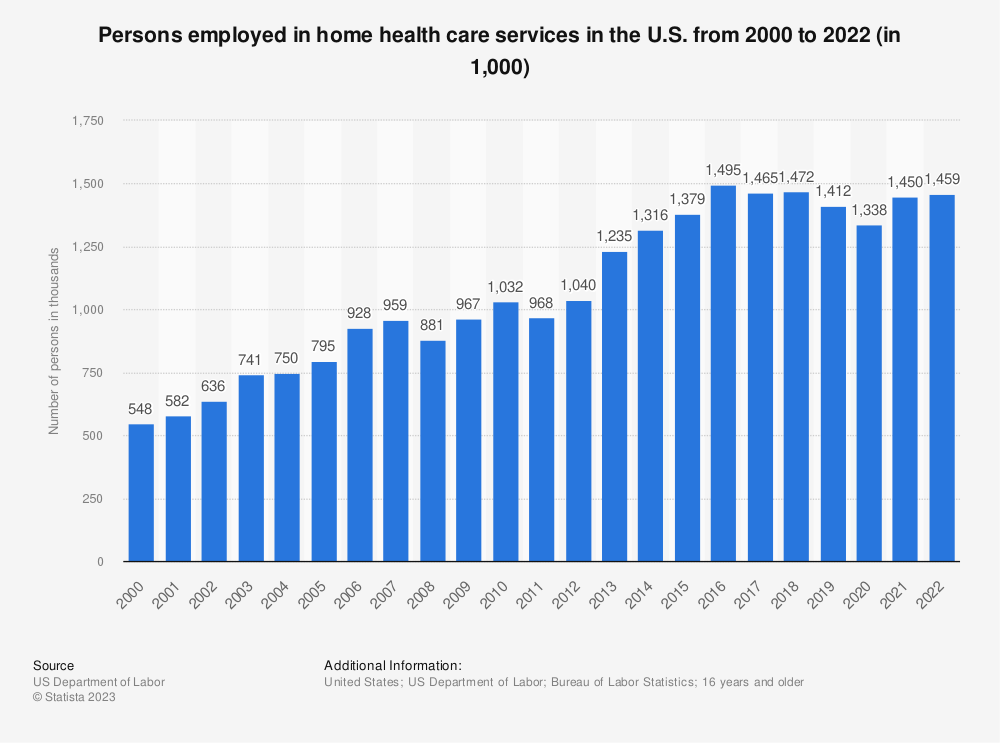

The USA has the largest home healthcare workforce. According to Statista, as of 2022, there were approximately 1,460,000 people employed in the home healthcare sector with 84.5% women and 15.5% men. Zippa puts the demographic breakdown at 35.6% whites, Black or African American at 24.0%, Hispanic or Latino at 23.4%, and Asian at 10.5%.

Source: Statista

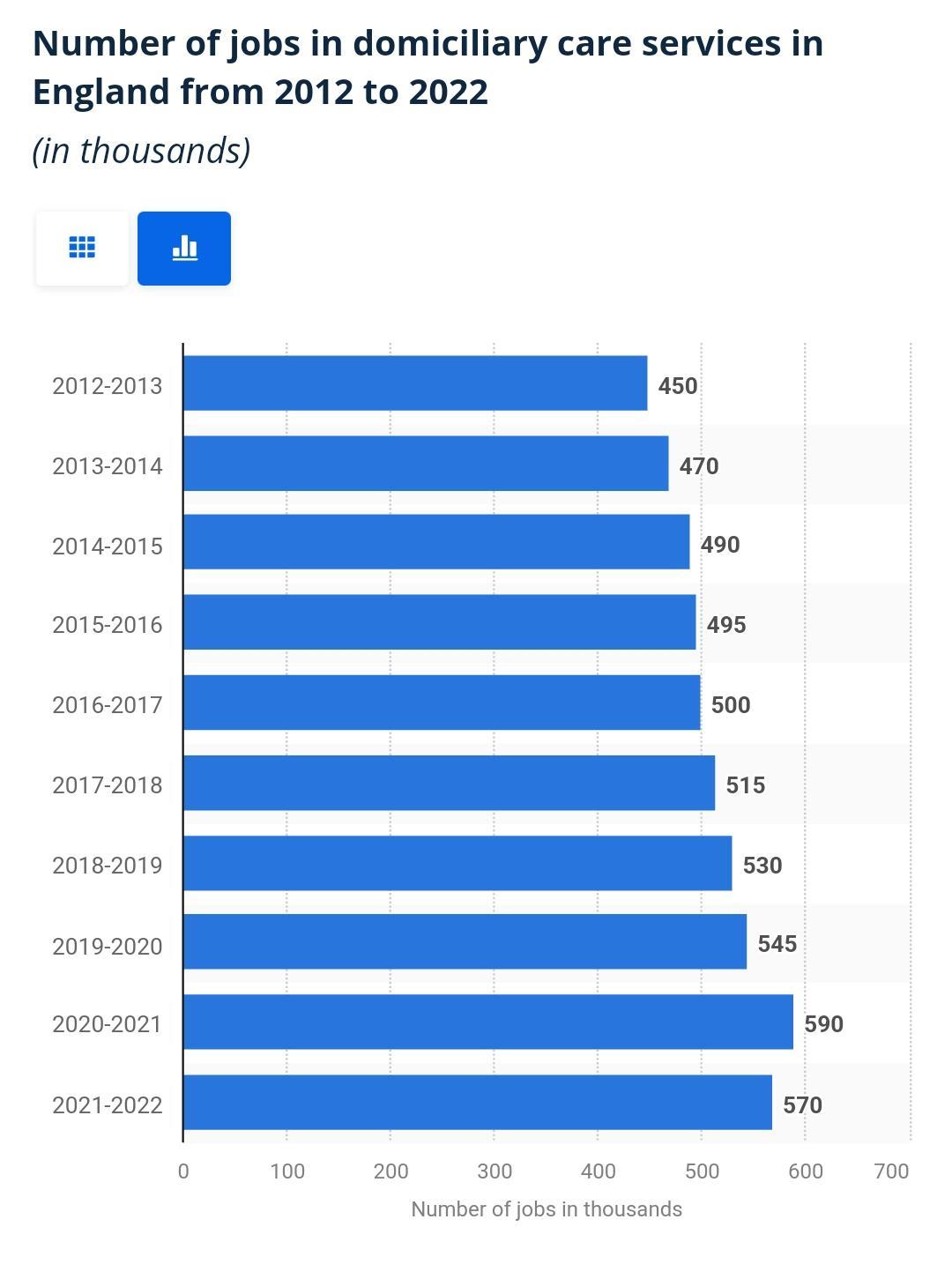

The UK follows with an estimated 570,000 domiciliary care workers in England and over 10,100 home care providers that are registered and regulated by the country’s regulatory body.

Source: Statista

Around 82% of workers in domiciliary care services identified as female and 18% identified as male. 27% of the workforce were aged 55 and above in 2022/23. This is an increase from 21% in 2016/17.

Similar research conducted by IBISWorld on Canada’s workforce between 2018 and 2023 indicated a potential of 83,854 employees in the industry.

Market Segmentation

The home healthcare industry in the United States is segmented into:

- Equipment: This is divided into Therapeutics, Diagnostics, and Mobility Assist equipment.

- Service: Classified as either skilled or unskilled home health care.

As of 2021, the services segment held the largest market share in terms of revenue. However, the equipment segment is expected to register the fastest growth during the forecast period due to the growing shift from hospital care to care at home, ease of treatment & diagnosis at home, and reduced costs.

The U.K. home healthcare industry is segmented into:

- Equipment Type: Consisting of Testing, Therapeutics, and Mobility Assist Equipment.

- Service: Skilled, Unskilled, Rehabilitation, Infusion Therapy, Hospice, and Palliative Services.

- By Indication: Cardiovascular Disorders, Diabetes, Wound Care, Cancer, Neurovascular Disorders and other indications.

The equipment and housekeeping supplies segments held a significant market share of 54% in the year 2019. The segment is likely to continue its dominance throughout the forecast period.

In Canada, segmentation is based on:

- Device Types: Diagnostic, Monitoring, Therapeutics, and Home Mobility Assist Devices.

- Services: Skilled, Unskilled, Rehabilitation, Infusion Therapy, Telehealth, and Telemedicine.

- Geographic Distribution: Ontario, Quebec, Alberta, and the rest of Canada.

Market Share Concentration

The concentration of market share is low across the three countries. The top four companies generate only about 40% of industry revenue. No player in the industry accounts for more than 7.0% of industry revenue. Globally, the industry’s top four largest players are expected to account for less than 20.0% of industry revenue in 2024 (IBISWorld).

In the US, no single company has a double-digit market share. The industry leaders generate less than 10% of the market share and less than $11 Billion of the total industry revenue. Additionally, because 90% of these companies are sole proprietorship businesses, they service a localized geographic region such as a city, county or state.

In the UK, City & County Healthcare Group Ltd is the national domiciliary care market leader and in Sheffield for instance, the agency is believed to have about 260 council-funded service users, giving it an 11% share of Sheffield’s council-funded domiciliary care market. There are other providers with a significant (>5%) market share.

In Canada, the homecare industry remains highly fragmented and ParaMed Home Health Care accounts for an estimated market share of 7.1% of the total industry revenue, followed by CBI Health Group at 1.8%.

Average Cost of Home HealthCare Services

As expected, each state in the US has its own average cost of care and charges. From a survey conducted by Genworth Financial, the national average comes to around $4,000 per month.

In the UK, the amount you pay for home care depends on your level of need and your assets. You should expect to pay an average of between £20 to £30 for the hourly cost of care at home.

Likewise in Canada, the average cost for home care is about 28 CAD to 35 CAD per hour. However, if you need more specialized care, you can hire a registered nurse (RN) or a registered practical nurse (RPN) at an average of 55-80 CAD per hour or 45-60 CAD per hour.

Government Funding and Support Programs

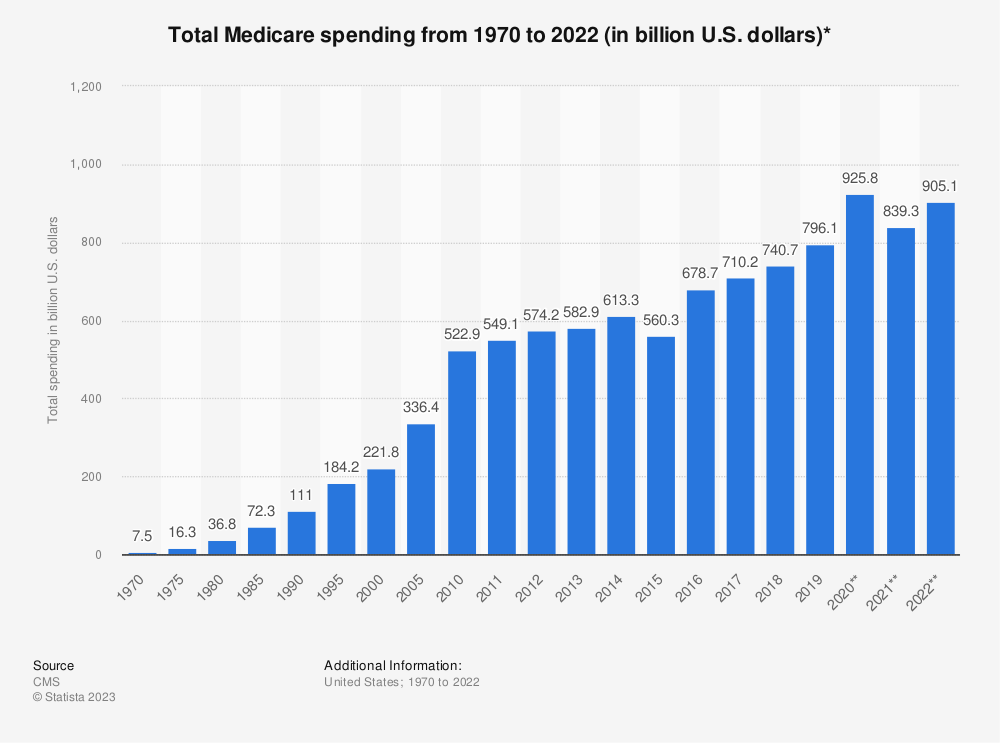

For U.S. residents there are different insurance programs for low-income persons that are state-specific. Government spending on services provided by home healthcare agencies increased by 6% in 2022 to $132.9 billion, an evident growth from 0.3% in 2021.

In the UK, if you’re eligible for NHS-funded nursing care (FNC) and your needs are primarily health-based, the NHS will cover the cost of the care and support you need in your home. This includes personal care such as help with washing and getting dressed. The government’s expenditure on adult social care rose in 2021/22 to £26.9 billion, an increase of 3.3% in cash terms and 3.8% in real terms over 2020/21.

While in Canada, most home and community care services are privately and publicly delivered by provincial, territorial, and municipal governments. Publicly-funded clients receive care in one of two ways – either through a contracted agency paid for by the government; or through a home care agency paid for by the client who receives a monthly stipend from the government to “shop” for home care that best meets their needs.

According to the Office of the Auditor General of Ontario, the total amount of funding to provide home care services was $2.7 billion. This is a 56% increase in funding and a 30% increase in clients compared to 2008/09.

Healthcare Policies and Regulations

Home healthcare policies and procedures vary drastically in the US because they are not all created equally. Each State, Medicare, Medicaid Program, Accrediting Body, etc. has its own set of standards to adhere to. It is important to distinguish every factor to ensure that your home healthcare policies and procedures are customized to meet these requirements.

Source: Statista

The UK’s Health Research Authority (HRA) and the four UK Health Departments are committed to an environment where safer, more efficient treatments and care are developed and tested through ethical and scientifically sound research for the benefit of patients, service users, and the public. The UK policy framework for health and social care research sets out principles of good practice in the management and conduct of health and social care research that take account of legal requirements and other standards.

In Canada, it is done differently. Home care services are not publicly insured through the Canada Health Act in the same way as hospital and physician services. Most home and community care services in Canada are delivered by provincial, territorial, and municipal governments.

Impact of COVID-19

During the pandemic in the US, there was a decrease in demand for home visits and this contributed to staffing challenges including lower wages and risk of COVID-19 infection.

According to a survey conducted in Massachusetts, 98.7% of home healthcare managers reported that clients canceled visits due to concern that health aides would expose them to COVID and 64.5% reported that family members assumed direct care tasks that had been provided by home health aides pre-pandemic. About 73.7% of these home healthcare managers reported that aides were concerned about going into homes and being infected by clients.

In the first year of the pandemic in the UK, there was a 50% reduction in the number of staff employed by home healthcare companies, thereby causing an increase in workload and working hours for the employed staff.

Also, in Canada during the first wave of the pandemic, personal care and therapies fell by 16% and 50%, respectively, whereas home nursing services did not significantly decline. However, by September 2020, all rates had recovered with nursing and therapies being higher than they have ever been. Service changes were largely consistent across the country, although the rural population experienced a larger decline in personal care and a smaller rebound in nursing.

Market Restraints

Major constraints across these three countries include:

- Common electrical problems associated with home equipment, software breakdown, and the complexity of machines, among others.

- Inadequate supply of skilled professionals to match up with the increasing demand for home healthcare services.

- Lack of awareness of the benefits of home healthcare, especially for those in rural areas.

- Health and safety hazards of home healthcare workers working in different environments.

Emerging Trends

One of the latest trends in home healthcare is the integration of Telehealth, which provides high-quality healthcare services without being hindered by geographical barriers. This innovative approach not only facilitates remote medical assistance but also allows for the identification and anticipation of potential health crises before they arise.

Also, the use of software technology (already a welcomed innovation) such as apps and digital tools to help with remote monitoring, vitals capturing, medication reminders, and abnormality alerts is significant in the evolution of home healthcare.

Patient Demographics

The percentage of people with chronic conditions increases with age. More than 90% of people in the United States older than 85 years have one or more chronic conditions.

Still in the U.S., the number of persons aged 65 years and above is estimated to increase to 71 million by 2030. This marks a notable increase from the 12.4% recorded in 2000 to a projected 19.6%. Also, the number of persons aged 80 years and above is expected to increase to 19.5 million in 2030. Nearly 70% of Americans who reach 65 will be unable to care for themselves at some point without assistance from Home Health Aides (HHAs), Registered Nurses (RNs), Licensed Practical Nurses (LPNs), Personal Care Aides (PCAs), and others.

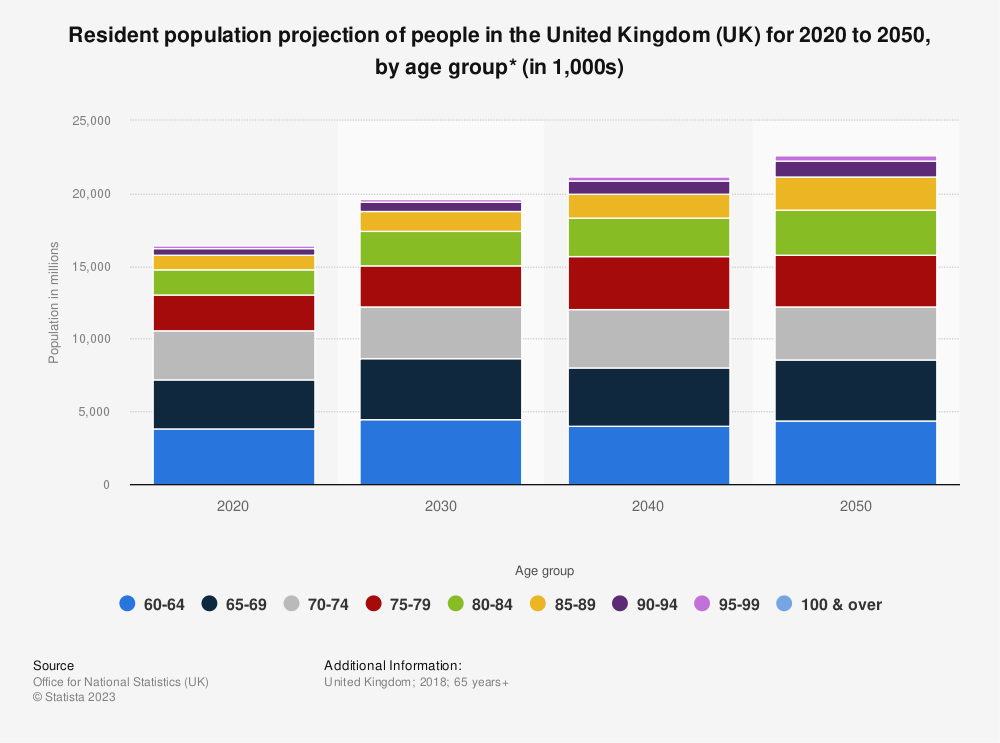

In the UK, the number of people aged 65 and over will surpass 15 million by 2030, by which time nearly 20% of the entire population will reach retirement age. As a result, there will be an increase in demand for in-home care and the importance of residential care, home care, and/or home healthcare in the UK’s healthcare system will be undeniable.

Source: Statista

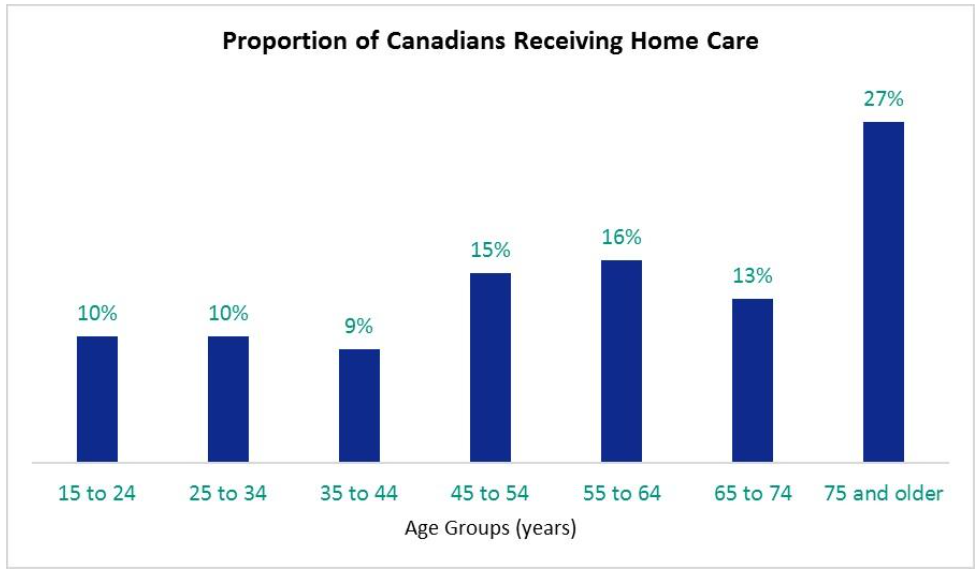

With previous research in Canada, home healthcare patients were mostly in their later years. About (27%) were in their mid-seventies or older, with just less than half of this group aged 85 years or above. However, 8% of Canadians aged 15 years and older received some form of home care which translates to roughly 2.2 million Canadians.

Source: Living Assistance Services

Key Performance Indicators (KPI) In the Home Healthcare Market

Knowing the right KPI to measure and track is very important to maintaining accountability in any industry. Tracking KPIs in the home healthcare market can help identify areas that require improvement and provide insight into an agency or industry’s productivity benchmark.

Some of the generally accepted KPIs are patient health outcomes, employee retention, customer satisfaction, average time to resolve service requests, cost per patient visit, referral rate, and expense management.

What The U.S. Can Learn From These Countries

While the stats and other information presented above are meant only for informational purposes, there are some crucial insights or lessons that the United States can glean from the home healthcare industries of the United Kingdom (UK) and Canada. They include:

- Equitable Healthcare: The U.S. will do very well to work on prioritizing equitable access to essential home healthcare services for its residents, regardless of their financial circumstances or insurance status.

- Integrated Care Approach: This approach adopted in the UK and Canada stands as a model for America to consider. It extends beyond medical care to include various other aspects of a person’s well-being, incorporating elements like medical treatment, rehabilitation, mental health support, and assistance with daily activities.

- Seamless Coordination And Communication: Promoting communication between healthcare providers can enhance patient outcomes, efficiency, and effectiveness while reducing duplication of services and leading to cost savings.

- Standardization and Regulation: Just as it is practiced in Canada, this can ensure consistent quality and safety standards across different regions and states and improve the overall reliability of home healthcare services, irrespective of which agency is providing them.

- Technology: The United States should be intentional in the adoption of technologies such as telehealth and remote monitoring. This practice, as seen in the UK and Canada, can significantly improve home healthcare delivery, expand access to care, and help create health plans that meet individual patient preferences.

- Financial Burden: If the U.S., which has the most expensive healthcare system in the world, starts making concerted efforts to significantly reduce the cost of healthcare for patients, it will not only drastically improve its home healthcare subsector but its entire health industry.

Final Thoughts

This comparative analysis of the home healthcare industry statistics in the U.S., UK, and Canada reveals both notable differences and valuable lessons for the U.S. These statistics highlight the value of examining healthcare systems beyond national borders by providing insight into how to identify best practices and areas for improvement.

This data allows the United States the opportunity to develop a more comprehensive and accessible home healthcare industry. By drawing inspiration from the experiences of the UK and Canada, it can improve the well-being of its citizens and strengthen the country’s overall healthcare system.